HUD Releases New Guidance for Manual Underwriting Changes

by: Anna DeSimone

On January 21, 2014, HUD published ML 2014-02: Manual Underwriting. The Mortgagee Letter provides policy guidance for revised manual underwriting requirements published in Final Federal Register Notice FR- 5595-N-01 on December 11, 2013. Please refer to my article published December 12, 2013 in the Compliance Monitor: FHA Manual Underwriting Changes Announced

This guidance is effective for case numbers assigned on or after April 21, 2014. Based on the Final Notice, the Mortgagee Letter explains maximum qualifying ratios for manually underwritten loans, and revises and clarifies the compensating factors that must be cited in order to exceed FHA’s standard qualifying ratios for manually underwritten loans.

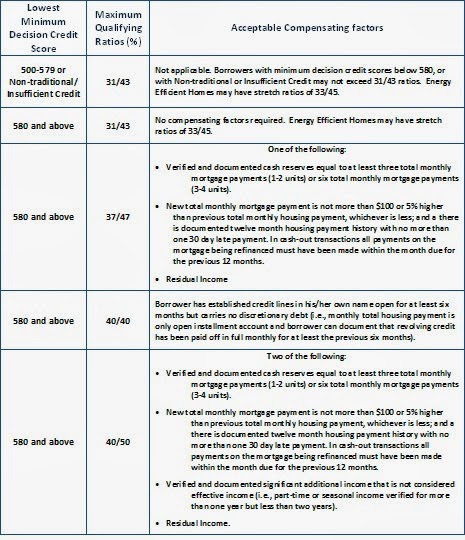

Maximum Qualifying Ratio Matrix

The maximum total monthly mortgage payment to gross effective income ratios and total monthly fixed payments to gross effective income ratios applicable to manually underwritten loans are summarized in the matrix below.

Manual Underwriting Matrix for Case Numbers Issued on or After April 21, 2014

(Click to enlarge)

Summary – FHA Guidance for Manually Underwritten Loans

The Mortgagee Letter addresses the following changes in underwriting guidance for manually underwritten loans:

-

maximum qualifying ratios for all manually underwritten loans based on the minimum decision credit score;

-

revised compensating factors that must be used in order to exceed FHA’s standard qualifying ratios; and

-

requirement for cash reserves equal to one or more total monthly mortgage payments for manually underwritten loans involving one and two unit properties.

Definition of Manually Underwritten Loans

Manually underwritten loans include:

-

loans involving borrowers without a credit score which were not scored against FHA’s TOTAL Scorecard;

-

loans receiving a Refer scoring recommendation from FHA’s TOTAL Scorecard; and

-

loans receiving an Accept scoring recommendation from FHA’s TOTAL Scorecard but which have been downgraded to a Refer by the underwriter.

When a loan receiving an Accept scoring recommendation is downgraded to a Refer, the loan must be underwritten in accordance with all provisions of this Mortgagee Letter.

Definition of Minimum Decision Credit Score

A minimum decision credit score is determined for each borrower according to the guidance provided in HUD Handbook 4155.1, Chapter 4, Section A.1.j. When three scores are available (one from each repository), the median (middle) value is used; when only two are available, the lesser of the two is chosen; when only one is available that score is used.

Where the loan involves multiple borrowers, the mortgagee must determine the minimum decision credit score for each borrower, and then select the lowest minimum decision credit score for all borrowers. Where the loan involves multiple borrowers and one or more of the borrowers do not have a credit score (non-traditional or insufficient credit), mortgagees shall select the lowest minimum decision credit score of the borrower(s) with credit score(s). Example: The borrower has a minimum decision credit score of 637. One co-borrower has a minimum decision credit score of 619 and the other co-borrower has no credit score. The minimum decision credit score of 619 must be used to determine the maximum ratios.

Definition of Reserves

Reserves are defined as:

-

the sum of verified and documented borrower funds; minus

-

the sum the borrower is required to pay at closing, including the cash investment, closing costs, prepaid expenses, any payoffs that are a condition of loan approval, and any other expense required to close the loan; but not including

-

the amount of cash taken at settlement in cash-out transactions or incidental cash received at settlement in other loan transactions, gift funds in excess of the amount required for the cash investment and other expenses, equity in another property, and borrowed funds from any source.

Reference: Refer to HUD Handbook 4155.1, Chapter 5, Section B for more information on acceptable sources and documentation standards for borrower funds.

Reserve Requirement

All manually underwritten loans must meet or exceed the following minimum reserve requirements:

-

1 and 2 Unit Properties. Reserves must equal or exceed one total monthly mortgage payment.

-

3 and 4 Unit Properties. Reserves must equal or exceed three total monthly mortgage payments.

This new policy replaces the current 2-month minimum reserve requirement for one and two unit properties for borrowers with insufficient credit.

Borrowers with Minimum Decision Credit Scores Below 580 or With Non-traditional or Insufficient Credit

The maximum allowable qualifying ratios for borrowers with minimum decision credit scores below 580 or with non-traditional or insufficient credit are as follows:

-

total monthly mortgage payment may not exceed 31% of gross effective monthly income (33% for Energy Efficient Homes); and

-

total monthly fixed payment may not exceed 43% of gross effective monthly income (45% for Energy Efficient Homes).

Borrowers with credit scores below 580 or with non-traditional or insufficient credit may not exceed the 31/43 ratios (33/45 for Energy Efficient Homes) regardless of whether they meet one or more compensating factors.

Pursuant to Handbook 4155.1, Chapter 4, Section C.3.c, the qualifying ratios for insufficient credit borrowers are computed using income only from borrowers occupying the property and obligated on the loan. Non-occupant co-borrower income may not be included. Income from non-occupant co-borrowers may be included in the ratios for non-traditional credit borrowers.

Borrowers with Minimum Decision Credit Scores of 580 or More and No Compensating Factors

The maximum allowable qualifying ratios for borrowers with minimum decision credit scores of 580 or more and no compensating factors are as follows:

-

total monthly mortgage payment may not exceed 31% of gross effective monthly income (33% for Energy Efficient Homes); and

-

total monthly fixed payment may not exceed 43% of gross effective monthly income (45% for Energy Efficient Homes).

Borrowers with Minimum Decision Credit Scores of 580 or More and One Compensating Factor

The maximum allowable qualifying ratios for borrowers with minimum decision credit scores of 580 or more provided they meet one of the compensating factors specified below are as follows:

-

total monthly mortgage payment may not exceed 37% of gross effective monthly income; and

-

total monthly fixed payment may not exceed 47% of gross effective monthly income.

Acceptable compensating factors are limited to the following:

-

Verified and documented cash reserves that equal or exceed three total monthly mortgage payments (one and two units) or that equal or exceed six total monthly mortgage payments (three and four units);

-

New total monthly mortgage payment is not more than $100 or 5% higher than previous total monthly housing payment, whichever is less, and there is a documented twelve month housing payment history with no more than one 30 day late payment. In cash-out transactions all payments on the mortgage being refinanced must have been made within the month due for the previous twelve months.

-

Residential income

Borrowers with Minimum Decision Credit Scores of 580 or More and Two Compensating Factors

The maximum allowable qualifying ratios for borrowers with minimum decision credit scores of 580 or more provided they meet two of the compensating factors specified below are as follows:

-

total monthly mortgage payment may not exceed 40% of gross effective monthly income; and

-

total monthly fixed payment may not exceed 50% of gross effective monthly income.

Acceptable compensating factors are limited to the following:

-

Verified and documented cash reserves that equal or exceed three total monthly mortgage payments (one and two units) or that equal or exceed six total monthly mortgage payments (three and four units);

-

New total monthly mortgage payment is not more than $100 or 5% higher than previous total monthly housing payment, whichever is less, and there is a documented twelve month housing payment history with no more than one 30 day late payment. In cash-out transactions all payments on the mortgage being refinanced must have been made within the month due for the previous twelve months.

-

Verified and documented significant additional income that is not considered effective income; and

-

Residual income.

Borrowers with Minimum Decision Credit Scores of 580 or More with No Discretionary Debt

The maximum allowable qualifying ratios for borrowers with minimum decision credit scores of 580 or more with established credit lines in their own name open for at least six months who carry no discretionary debt (housing payment is only account with an outstanding balance and borrower can document that revolving credit has been paid off in full monthly for at least the previous six months) are as follows:

-

total monthly mortgage payment may not exceed 40% of gross effective monthly income; and

-

total monthly fixed payment may not exceed 40% of gross effective monthly income.

For borrowers meeting this criterion no other compensating factors are required.

Recording Compensating Factors

Compensating factors cited to support the underwriting decision must be recorded in the Underwriter Comments section of Form HUD-92900-LT, FHA Loan Underwriting and Transmittal Summary. Documentation supporting the compensating factors cited must be included in the endorsement case binder including, if applicable, a worksheet attached to Form 92900-LT reflecting the calculation of residual income.

Energy Efficient Homes

Current policy allows borrowers who are manually underwritten with homes built or retrofitted to exceed the applicable IECC standard including Energy Efficient Mortgages to exceed the 31/43 ratios (33/45 stretch ratios). These borrowers may be eligible for ratios in excess of the 33/45 stretch ratios but not exceeding 37 and/or 47, only if they have a minimum decision credit score of 580 or higher and meet at least any one of the compensating factors specified on page 6 of this Mortgagee Letter. Ratios exceeding 37/47 (not to exceed 40 and/or 50) may be approved only if they have a minimum decision credit score of 580 or higher and meet at least any two of the compensating factors specified on page 7 of this Mortgagee Letter.

Example: A borrower with a credit score of 570 is purchasing an Energy Efficient Home. The maximum allowable ratios are 33/45.

Example: A borrower with a credit score of 590 and one compensating factor is purchasing an Energy Efficient Home. The maximum allowable ratios are 37/47.

The Letter also explains the new reserve requirement for manually underwritten loans for one and two unit properties. This Mortgagee Letter is not applicable to:

-

Non-credit qualifying FHA to FHA streamline refinance mortgages;

-

Refinances of Borrowers in Negative Equity Positions (ADP Codes 821, 822, 831 832);

-

Section 255 Home Equity Conversion Mortgages; or

-

Title I loans.

Please refer to the mortgagee letter for additional information regarding “Documenting Acceptable Compensating Factors” and the guidelines for underwriting VA Mortgages.

About the Author

Anna DeSimone is President and Founder of Bankers Advisory, Inc. She can be reached at anna@bankersadvisory.com

Anna DeSimone founded Bankers Advisory in 1986 and is a nationally recognized authority in residential mortgage lending. She has received numerous industry awards and has authored more than 40 best practices guides and hundreds of articles.

Comments are closed.